How Much Down Payment for Land Is Typically Required?

Ross AmatoThe down payment for raw land depends entirely on how you finance it. For a traditional bank loan, expect to pay 20% to 50% of the purchase price upfront. With seller financing, that figure often drops significantly, typically ranging from 0% to 20%. The path you choose determines the cash you need to get started.

This guide is for prospective buyers trying to understand the real upfront costs of purchasing vacant land. We will explain why bank requirements are so high, what factors influence the amount you'll pay, and how seller financing makes land ownership more accessible. This article covers financing for raw land purchases and does not cover construction loans or home mortgages.

Why the Wide Range?

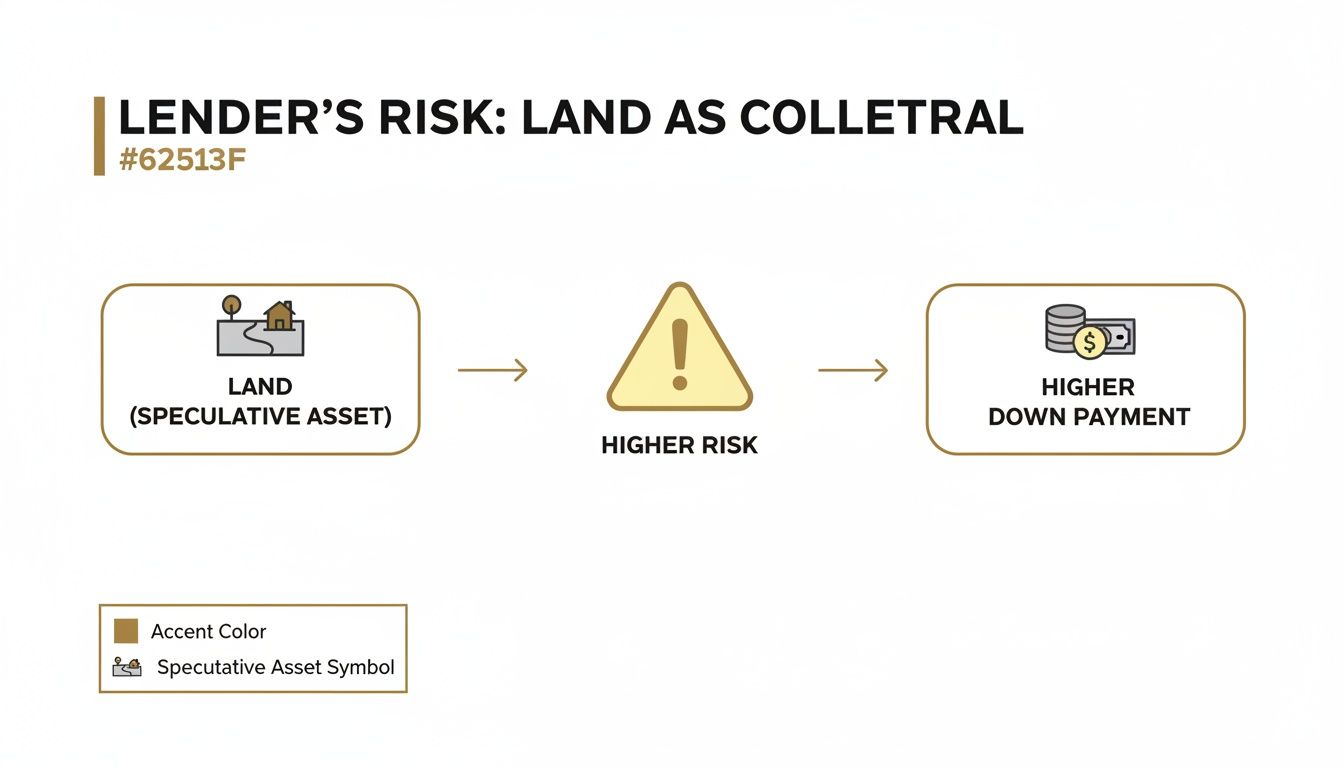

Unlike a standard mortgage for a house, financing raw land is seen as a bigger risk by most lenders. From their perspective, vacant land lacks a house to serve as stable, immediate collateral. If a borrower defaults, an empty lot is much harder for a bank to sell than a home.

This higher risk translates directly into a larger required down payment, ensuring you have significant "skin in the game." The amount is almost always calculated as a percentage of the land’s price, which is a key part of understanding the Loan to Value Ratio (LVR). Your financing path is the single biggest factor influencing this percentage.

Typical Down Payment for Land at a Glance

To make it simple, here’s a quick comparison of what to expect depending on your financing source.

| Financing Type | Typical Down Payment Range | Best For |

|---|---|---|

| Traditional Bank Loan | 20% – 50% | Buyers with excellent credit, a detailed building plan, and significant cash reserves. |

| Seller/Owner Financing | 0% – 20% | Buyers looking for flexibility, lower upfront costs, and a simpler approval process. |

The difference is substantial.

- Bank Financing: Banks are conservative. They view raw land as a speculative investment that can take a long time to sell. To mitigate this risk, they demand a substantial down payment. You will rarely see a bank ask for less than 20%, and for rural or completely undeveloped parcels, that number can easily climb toward 50%.

- Seller Financing: When you work directly with the owner, the dynamic changes. The seller’s goal is to sell their property, not to meet a bank’s strict lending criteria. This usually means they are more flexible, often leading to much lower down payments and making land ownership a reality for more people.

Why Bank Down Payments for Land Are So High

Have you ever looked into a loan for a piece of raw land and wondered why the process feels so different from buying a house? It all boils down to a single word: risk. In the eyes of a traditional lender, a house is a predictable asset. Vacant land, on the other hand, is a speculative one.

A house is tangible collateral that is easy to value and, if necessary, sell. It can generate rental income, and its market value is usually straightforward to determine. Raw land is a different challenge. It doesn't produce income, its value can be difficult to assess, and it often takes much longer to sell, especially in a slow market. This uncertainty makes traditional lenders cautious.

Seeing Things from the Lender's Side

For a bank, collateral is everything—it’s their safety net if a borrower stops making payments. Since raw land is seen as less stable collateral than a home, lenders protect themselves by requiring a larger commitment from you, the buyer.

A higher down payment does two key things for a lender:

- It lowers their exposure. The more cash you put down, the less money they have to lend, which directly cuts their potential loss if the loan defaults.

- It demonstrates commitment. A large down payment shows you have "skin in the game," making you a more reliable borrower who is less likely to walk away from the investment.

This isn’t unique to land; it’s a trend across real estate. The National Association of Realtors recently reported that the median down payment for all home buyers was 19%. Repeat buyers put down a median of 23%—the highest since 2003—showing that lenders are tightening standards everywhere. You can check out the full report on home buyer trends from NAR for more data.

A Common Misconception: Many buyers assume that an excellent credit score guarantees a low-down-payment deal on land, similar to a home mortgage. The truth is, for banks, the nature of the asset—the raw land itself—is what drives the high down payment requirement. The property's speculative quality often matters more than a perfect credit history.

This is why learning how much down payment for land is needed often comes as a surprise. It also explains why alternative paths, like seller financing, have become a popular solution for buyers who want to get started without a huge upfront cost.

Key Factors That Influence Your Land Down Payment

The down payment on land isn’t an arbitrary number. It’s the result of a risk calculation by the lender or seller. Understanding these factors is key to knowing why one property might require 5% down, while another demands 40%. The most significant factor is your financing source.

When you go to a traditional bank or credit union, you must play by their rigid rules. Seller financing, however, is a direct agreement between you and the landowner, allowing for much more flexibility, especially on the down payment.

Property Characteristics and Location

The land itself heavily influences the down payment. Lenders prefer properties that are less risky and would be easier to sell in case of foreclosure.

Here's what they focus on:

- Access and Utilities: Is there a legal, established road to the property? Are public utilities like water, sewer, and electricity already available? A lot that is ready to build on is a much safer bet than a remote, off-grid parcel. For example, a property in Apache County, Arizona with dirt road access and no utilities will almost always require a higher down payment from a bank than a suburban lot with paved access.

- Zoning and Land Use: Land already zoned for residential use is a known quantity. A parcel with vague agricultural or mixed-use zoning presents more uncertainty.

- Location: A lot in a growing suburban area will seem safer to a lender than a rural parcel hours from the nearest town, often resulting in a lower down payment requirement.

Your Personal Financial Situation

Your financial health is critical in a traditional bank loan process, though seller financing often skips this step. Lenders will pull your credit score and review your financial history. A strong score demonstrates a track record of responsible debt management and might earn you a lower down payment.

If your credit is weak, a bank might demand 50% or more down or deny the loan altogether. They also want to see proof of stable income and a healthy debt-to-income ratio to ensure you can handle the monthly payments.

The Impact of Soaring Property Values

The broader real estate market also plays a significant role. When prices are high, the dollar amount needed for a down payment can become a massive hurdle, even if the percentage is reasonable.

For example, the median home price in the U.S. recently hit a record $414,000. A common 19% down payment on that figure comes out to $78,660 in cash. You can dig into more recent trends in real estate statistics to see just how much the market has shifted.

Down Payment Examples: Real-World Scenarios

Let's break down how percentages translate into real dollars. Seeing what 20% or 30% actually means for your bank account provides a much clearer picture of the cash you'll need upfront.

Scenario 1: The Traditional Bank Loan

Imagine you've found a $50,000 parcel zoned for residential use with utilities at the property line, making it a lower-risk asset for a lender. You go to a local bank, which approves you for a land loan but requires a 30% down payment.

Here’s the math:

- Purchase Price: $50,000

- Down Payment Percentage: 30%

- Calculation: $50,000 x 0.30 = $15,000

You would need $15,000 in cash for the down payment alone, not including closing costs. For most people, saving this amount is a major barrier.

Scenario 2: The Seller Financing Route

Now, consider a different approach. You find a remote 5-acre property listed for $20,000 through a seller financing company. The owner offers flexible terms requiring only a 10% down payment.

The numbers become much more manageable:

- Purchase Price: $20,000

- Down Payment Percentage: 10%

- Calculation: $20,000 x 0.10 = $2,000

Your upfront cost drops to just $2,000, bringing land ownership within reach much sooner. It's also worth noting that even traditional down payments are climbing. According to Realtor.com, the median down payment recently hit 14.4%, which comes out to about $30,400—more than double what it was in 2019. You can see the full report on down payment trends here.

Scenario 3: Special Low-Money-Down Offers

To make land even more accessible, many sellers—including Dollar Land Store—offer promotions like "$1 Down" or "$99 Down" deals. These are designed to remove the initial financial barrier almost completely.

Buyer Insight: These offers are legitimate, but it's important to understand how they work. The ultra-low down payment is usually paired with a one-time, non-refundable document fee (e.g., $249) that covers the administrative work of setting up your contract.

So, for a $1 down deal with a $249 document fee, your total out-of-pocket cost is just $250. This is the most accessible path to land ownership. The trade-off is that the total purchase price or interest rate might be slightly higher to balance the seller's risk. It’s a choice between maximum accessibility now and a potentially higher total cost later.

Risks & Limitations of a Low Down Payment

While a low down payment makes owning land highly accessible, it’s important to understand the full picture. It’s a trade-off that shifts the financial weight from day one to the life of your agreement. A smaller down payment always means a larger loan balance.

This larger balance typically leads to higher monthly payments and more total interest paid over time. You are trading a lower upfront cost for a higher total cost. This structure is designed for accessibility, not for long-term savings.

The Risk of Negative Equity

A low down payment increases the risk of being "upside down" or having negative equity, which occurs if the property's market value drops below what you owe. This can limit your options if you need to sell quickly. With very little equity to start, you have greater financial exposure to market fluctuations. This is a common risk with any real estate purchase using minimal money down.

A Realistic Scenario: Imagine you put $250 down on a $15,000 property. Your initial equity is less than 2%. If the market softens and similar lots start selling for $14,000, you would still owe nearly the full $15,000. This would put you in a negative equity position until you make enough payments to build equity.

When a Low Down Payment Isn't a Good Fit

A low down payment is an excellent tool if your primary goal is to secure a property now and you are comfortable with the monthly payments. However, it may not be the best choice if your budget is tight or you plan to seek a construction loan soon, as lenders prefer to see more equity. Putting down a larger payment might be the smarter long-term move in these situations.

Beyond the down payment, conducting your own essential real estate due diligence is the best way to verify property details and uncover potential issues.

The Dollar Land Store Context: Our Approach to Down Payments

At Dollar Land Store, our process is built around simple, transparent seller financing. We founded our business to help people own land without the hurdles of traditional bank loans. So, when it comes to how much down payment for land you need, we’ve made the answer as straightforward as possible.

We structured our agreements to move away from the 20-50% down payments banks demand. Instead, we offer much lower upfront costs, including frequent $1 down promotions. The only other upfront cost is a single, one-time document fee to set everything up. This model removes the single biggest barrier for most aspiring landowners.

Our Agreement for Sale Process

We use a clear contract called an Agreement for Sale. It’s a plain-language document that outlines the purchase price, your monthly payment, the agreement term, and all responsibilities. There are no banks, no credit checks, and no hidden surprises.

This entire model is about making land ownership sustainable and achievable. You can learn more in our guide on how seller financing paves the road to land ownership for you.

To ensure we can continue offering these terms, our agreement includes a few important ground rules. These are not meant to be restrictive; they exist to protect the property as collateral during the financing term, which benefits both buyer and seller.

- No Building Before Payoff: You cannot build permanent structures or make major changes to the land until it is fully paid off and the deed is in your name.

- No Occupancy Before Payoff: Living on the property, including long-term stays in an RV, is not permitted until you have made your final payment.

- Buyer Responsibility for Taxes: As the equitable owner, you are responsible for paying the annual property taxes directly to the county.

These rules ensure the land remains viable collateral, allowing us to keep land affordable and offer low down payments to everyone.

Your Next Steps

Understanding how much down payment is required for land is the first step toward making a confident purchase. Whether you choose a traditional loan or the flexibility of seller financing, knowing the numbers empowers you to plan effectively.

If the accessibility of a low down payment aligns with your goals, we invite you to explore our available properties.

- View our land listings

- Learn more about our seller financing process

- Contact us with any questions