A Beginner's Guide to Buying Plots of Land: Evaluation, Financing, and Due Diligence

Ross AmatoThinking about buying your first plot of land is a significant step toward owning a real, tangible asset. This guide is designed to provide a clear path for first-time buyers, cutting through the complexity of land transactions. We'll walk you through the essential steps, from browsing listings to understanding the paperwork.

Our focus is on the practical details that protect your investment and ensure the land you choose aligns with your goals—whether for recreation, a future home, or a long-term asset.

Your Practical Roadmap to Land Ownership

Buying a plot of land is fundamentally different from buying a house. With no structure to inspect, your entire focus shifts to the property itself: its location, what you are legally permitted to do on it, and its physical characteristics.

For beginners, this can feel unfamiliar, but the process follows a logical sequence. This guide will serve as your playbook for confidently purchasing a plot of land, particularly the kind of rural and undeveloped parcels that are often most accessible. We will address common questions about evaluating a property’s potential and explain what "due diligence" means in practice. We will also explore how options like seller financing can make land ownership possible without a traditional bank loan.

The Land Buying Journey

The process of buying land is best approached as a series of distinct phases. Each phase builds on the last, and rushing through the initial steps can lead to costly mistakes. A successful purchase isn't about finding the cheapest lot; it’s about finding the right lot for your specific needs and budget.

Knowing this roadmap helps you stay organized and make informed decisions from start to finish.

Key Stages in the Land Buying Process

The journey can be broken down into four primary stages:

| Phase | Key Objective | Common Question for Beginners |

|---|---|---|

| Phase 1: Evaluation | Assess the land's physical and legal suitability for your goals. | "Can I actually use this land for what I have in mind?" |

| Phase 2: Due Diligence | Verify all claims about the property and uncover potential issues. | "Are there any hidden problems, like liens or access disputes?" |

| Phase 3: Financing | Secure the funds needed for the purchase, often outside of traditional banks. | "How can I afford this if I don't have all the cash upfront?" |

| Phase 4: Closing | Finalize the legal transfer of ownership and complete all paperwork. | "What documents do I need to sign to make the land officially mine?" |

Understanding these phases demystifies the entire process, turning a potentially daunting task into a series of manageable steps.

Setting Realistic Expectations

Buying plots of land, especially raw or rural land, requires a researcher's mindset. Your primary responsibility is to confirm every critical detail with the appropriate authorities, which almost always begins with the county’s planning and zoning department.

Important Note: Never assume anything about a property. Whether it’s road access, zoning regulations, or utility availability, you must verify everything yourself. This is the single most important part of the land buying process.

This guide provides the knowledge you need to ask the right questions and find the correct answers. By following a structured approach, you can navigate the process with confidence and turn the dream of owning land into a reality.

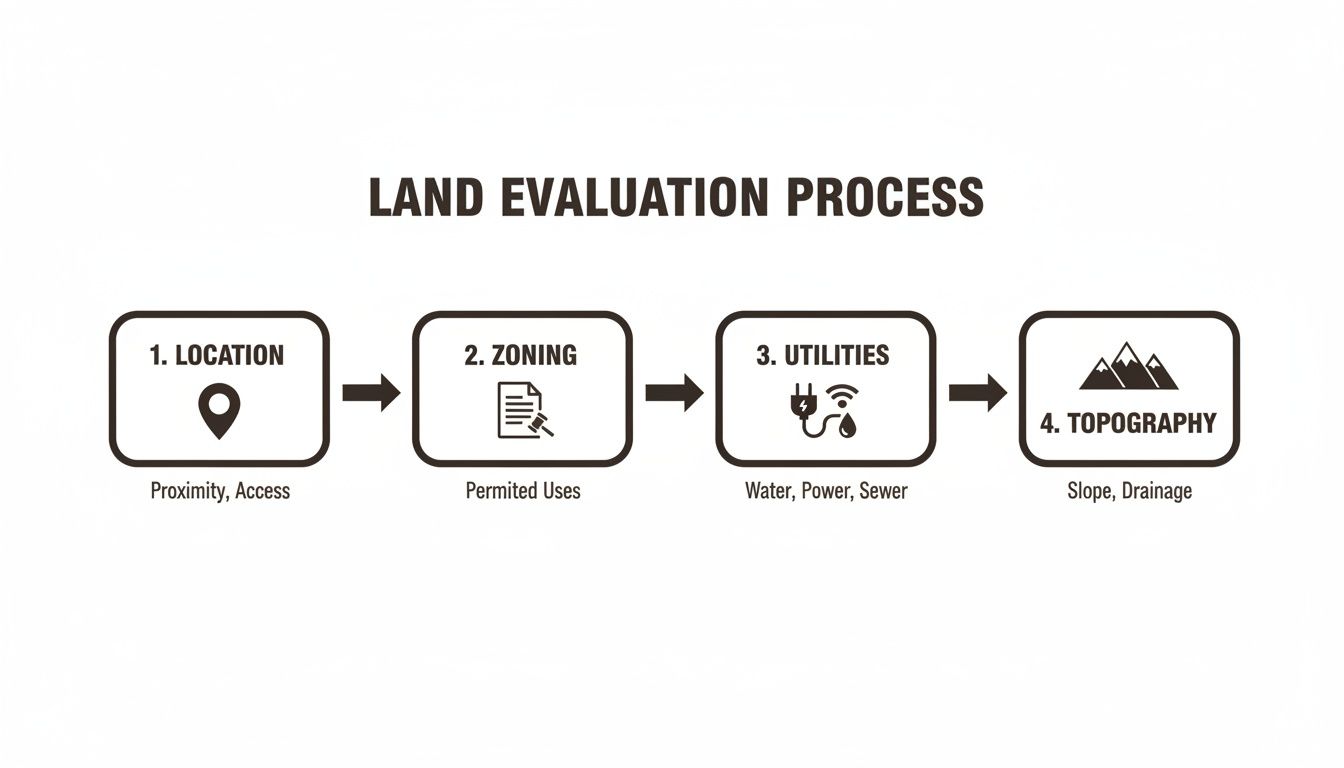

Evaluating Land: The Four Pillars of a Smart Purchase

Before considering the price of a property, it's crucial to perform thorough research. This evaluation phase is where you move beyond the online photos and investigate the details that determine whether a property is a sound investment or a potential liability.

A smart land purchase comes down to investigating four key areas. Getting these right will help you avoid surprises and ensure the land you buy fits your plans.

Pillar 1: Location and Access

The real estate mantra "location, location, location" is all about access when it comes to raw land. It's not just about finding the property on a map; it's about your legal and physical ability to get to it.

- Legal Access: This is a documented right to reach your property, typically via a public road or a recorded easement allowing you to cross a neighbor's land. Without legal access, a property is considered "landlocked," which can significantly reduce its value and usability.

- Physical Access: This refers to the actual condition of the road. Is it paved, gravel, or a dirt track that may become impassable in certain weather? A line on a map does not guarantee a road is usable year-round.

You can begin your research from home using tools like Google Earth and county GIS (Geographic Information System) maps to get a sense of the terrain, surrounding area, and the route to the property.

Pillar 2: Zoning and Permitted Use

This is a critical, non-negotiable step. Zoning regulations are the official county rules that dictate what you can and cannot do with your land. A common mistake for first-time buyers is assuming they can build a home, park an RV, or start a farm without confirming the rules.

You must contact the county's Planning and Zoning department directly. Ask for the property's specific zoning designation, which might be:

- Agricultural (AG): Typically for farming or ranching, often with restrictions on residential structures.

- Rural Residential (RR): Allows for homes on larger lots but may have specific rules about temporary structures like RVs or tiny homes.

- Recreational (REC): May permit seasonal camping but could prohibit the construction of a permanent dwelling.

Disclaimer: Never rely solely on a seller's advertisement for information on permitted uses. The county has the final authority. A direct phone call can prevent you from purchasing land you cannot use as intended.

Pillar 3: Utilities and Resources

Much of the affordable, rural land available is "off-grid," meaning it lacks connections to municipal water, power, or sewer systems. You need to understand the financial and practical implications of this.

- Water: Your options may include drilling a well (which can be a significant expense), hauling water to a storage tank, or implementing a rainwater collection system.

- Power: Solar energy is a common solution for off-grid properties. Other options include generators or, in some areas, wind power.

- Waste: A septic system is standard for off-grid properties. This requires a soil percolation ("perc") test to ensure proper drainage and can be a major installation cost.

Clarifying these three elements will help you create a realistic budget that extends beyond the land's purchase price. For more detail, see our guide on what to look for when buying land.

Pillar 4: Topography and Environment

Finally, assess the physical characteristics of the land. The "lay of the land" can significantly impact your plans. A steep, rocky slope may offer great views but could make building a driveway or foundation prohibitively expensive.

Use topographic maps to review elevation and slopes. You should also check for environmental factors. FEMA provides flood maps that indicate if a property is in a high-risk flood zone, which can affect construction and insurance. Consider other factors like soil quality, dense vegetation, or proximity to protected areas.

Some investors take this a step further by conducting a real estate development feasibility study to analyze long-term potential. By thoroughly investigating these four pillars, you are not just buying land; you are making an informed investment.

Your Due Diligence Checklist for Buying Land

Once you've found a property that passes your initial evaluation, it's time to begin due diligence. This is the verification phase where you confirm every detail, uncover potential issues, and ensure the land is exactly what the seller represents it to be. Skipping this step is a significant risk.

Title Verification and Liens

First, you must confirm that the seller has the legal right to sell the property and that it is free of financial encumbrances.

- Preliminary Title Check: You can often perform a basic search on the county recorder’s website. This can help you spot obvious red flags like existing mortgages or tax liens.

- Professional Title Search: For complete assurance, a title company can conduct a professional title search. They will research the property's history to ensure the "chain of title" is clear, meaning no one else has a claim to your land.

Key Concept: A clear title is your legal proof of sole ownership, free from past debts or ownership disputes. It is an essential component of a secure land transaction.

This step ensures the ownership transfer is clean and legally sound. Our article on what to ask when buying land provides a comprehensive list of questions for this stage.

The flowchart below illustrates the foundational checks that should be completed before this phase.

If a property passes these initial four tests, it's worth investing the time in the deeper due diligence steps that follow.

Surveys and Property Boundaries

A listing might state a property is five acres, but a property survey is the only way to be certain of its exact boundaries. A survey is crucial for preventing future disputes with neighbors.

There are several types of surveys:

- Boundary Survey: This is the most common type for raw land. A licensed surveyor physically marks the corners and property lines.

- ALTA/NSPS Land Title Survey: This is a more detailed and expensive survey, typically used for commercial transactions, that shows boundaries, easements, improvements, and utility lines.

For most raw land purchases, a boundary survey is sufficient. While it is an upfront cost, it provides invaluable peace of mind. To better understand the official layout of your land, you can learn more from a comprehensive guide to site plans.

Environmental and Site Checks

Finally, check for environmental issues that could limit land use or pose health risks. Public records make this process manageable.

Start by checking online databases from the Environmental Protection Agency (EPA) for any nearby hazardous sites. You should also consult FEMA flood maps to determine if the property is in a high-risk flood zone. Additionally, verify that no part of the land is designated as protected wetlands, which would carry significant building restrictions.

These checks are about removing uncertainty. By methodically working through this due diligence checklist, you can move forward with confidence, knowing there are no surprises waiting for you after the purchase is complete.

Financing Your Land Purchase Without a Bank

One of the first challenges many buyers encounter is that financing raw land is different from getting a home mortgage. Traditional banks are often hesitant to lend on undeveloped property, which can seem like a barrier.

However, many buyers successfully purchase land without a bank. While some pay with cash, a common and accessible path is through seller financing.

How Seller Financing Works

Seller financing, also known as owner financing, is a straightforward arrangement. Instead of a bank, the person or company selling the land acts as the lender. You make payments directly to the seller over an agreed-upon term.

This process eliminates the need for bank approvals, extensive paperwork, and strict credit requirements. For buyers who don't have a large amount of cash available or a perfect credit history, it is often the most practical way to purchase land.

Key Concept: With seller financing, the property itself serves as collateral for the loan. The seller provides the credit, which makes land ownership accessible to a broader range of buyers.

The process is typically faster and simpler than a traditional loan, involving a direct agreement between the buyer and seller.

A Hypothetical Example of Financing Terms

To illustrate, imagine a parcel of land listed for $10,000 with seller financing available. The terms might look like this:

- Purchase Price: $10,000

- Down Payment: A modest initial payment, often just a few hundred dollars.

- Document Fee: A one-time fee, for example $250, to cover the preparation of legal documents like the contract for sale and promissory note.

- Interest Rate: A fixed rate charged on the loan balance, such as 9%.

- Loan Term: The length of the repayment period, for instance, 10 years (120 months).

After the down payment and document fee, the monthly payment is calculated based on the remaining balance. These payments are typically fixed, allowing for predictable monthly budgeting. For more information, see our guide to owner-financed land for sale.

Why Many Land Buyers Prefer Seller Financing

The appeal of seller financing extends beyond simply avoiding banks. A key advantage is that sellers like Dollar Land Store often do not perform credit checks. This opens the door to land ownership for individuals who are building their credit or may not meet traditional lending criteria.

The terms are clear and disclosed upfront in the contract, including the interest rate, payment schedule, and total cost. This simplicity and transparency make it an ideal option for many first-time land buyers.

What This Means for Buyers

For a first-time land buyer, the process is different from buying a house, but it is not necessarily more difficult. Your focus simply shifts to different priorities. With no home to inspect, your attention turns to the land itself.

Your top priorities are verifying legal access, confirming county zoning rules, and understanding utility options. Addressing these three areas thoroughly is the foundation of a smart purchase.

The financing process is also different. Instead of a traditional mortgage, you will likely use cash or seller financing. This is often an advantage for first-time buyers, as seller financing can remove barriers like credit scores or large down payments. However, this accessibility requires you to be diligent. You must read every part of the financing agreement—from the interest rate to the payment schedule—to ensure it fits your budget.

Buying land is an attainable goal. The key is to replace assumptions with verification. By methodically checking the details, understanding your financing, and working with a transparent seller, you can move forward with confidence. A few phone calls to the county planning department and a clear understanding of your purchase contract are your most powerful tools.

Why Consider Dollar Land Store?

When you're buying your first piece of land, the seller you choose matters. Dollar Land Store is not a real estate agency or broker; we are the direct owner of every parcel we sell.

This direct-seller model allows us to eliminate middlemen, commissions, and unnecessary complexity. Our focus is on offering affordable raw land with a straightforward seller financing process designed for first-time buyers. Our goal is to make land ownership accessible and transparent.

A Simple Path to Land Ownership

Our entire process is built on clarity and ease. By handling everything in-house, we can offer terms that make sense for new land buyers.

Most of our properties feature:

- Low Down Payments: Get started without needing a large amount of cash upfront.

- No Credit Checks: We don't believe your financial history should prevent you from owning land.

- Affordable Monthly Payments: We offer financing plans designed to fit a realistic budget.

- A Fast and Simple Process: We have streamlined our procedures to help you secure your land and finalize the contract quickly.

Every property listing provides clear, honest details, including location, acreage, and precise financing terms, so you can make an informed decision. You can learn more about our company and approach on our About Us page.

The appeal of land as a tangible asset continues to grow. A recent analysis highlights this trend, noting that foreign-held U.S. agricultural land increased by over 20 million acres between 2010 and 2023, underscoring the long-term value people see in owning land.

Buyer Guidance and Next Steps

Now it is time to transition from reading and researching to taking action. The best way to begin is by browsing available properties. This will give you a practical feel for what is available in terms of acreage, location, and price.

Make a Shortlist and Begin Your Research

As you browse, select two or three parcels that catch your interest. Apply what you've learned in this guide: check the access, look up the zoning, and research the utility situation. This is how you build practical knowledge and confidence.

If you are considering seller financing, this is also the time to review the terms. A trustworthy seller will clearly explain the numbers without pressure or confusing jargon. Ask questions until you are 100% clear on all aspects of the agreement.

It all boils down to three steps: explore your options, do your own research, and ensure you understand the financing. Following these steps will help you move confidently toward finding the right piece of land.

Common Questions from First-Time Land Buyers

Here are answers to some of the most common questions we receive from people who are new to buying land.

What are the real costs besides the purchase price?

The purchase price is the starting point. It is wise to budget for other potential costs. For example, a property survey can range from $500 to $2,000 but provides certainty about your boundaries. Title insurance is another expense that offers peace of mind. Remember to account for annual property taxes, which vary by county. If you plan to develop the land, get local quotes for major expenses like installing a well, a septic system, or connecting to the power grid.

Can I start living on my land immediately?

The answer depends entirely on local county regulations. Some counties have lenient rules, while others have strict zoning laws that may prohibit living in an RV or tiny home without a permanent residence or an active building permit.

Important: Always call the county's planning and zoning department for a final answer regarding your specific parcel. This single phone call can prevent significant legal and financial issues.

How does seller financing affect my credit score?

In most cases, it doesn't. Seller financing is a private agreement between the buyer and the seller. Since companies like Dollar Land Store often do not perform credit checks to qualify buyers, we typically do not report payment histories to the major credit bureaus. While this means it won't help build your credit history, it also means a low credit score doesn't prevent you from owning land.

Is buying affordable rural land a good investment?

For many people, yes. Historically, land has been a stable long-term asset that can hold its value and serve as a hedge against inflation. The investment potential often depends on factors like location, road access, and regional growth. However, many people buy land for personal use—as a recreational getaway, a family camping spot, or a quiet retreat. For these buyers, any future appreciation in value is an added benefit to their lifestyle investment.

The team at Dollar Land Store is here to help make the land buying process simple and to answer any questions you may have.