How to Buy Land with No Money Down: A Practical Guide

Ross AmatoThe dream of owning a piece of land—a place to invest, camp, or one day build—can feel out of reach, especially if you don't have a large sum of cash saved for a down payment. The good news is, you don't always need one. It is possible to buy land with no money down using smart strategies like seller financing, a method that bypasses traditional bank loans and makes land ownership accessible to almost anyone, regardless of their savings account balance.

This guide explains how these deals work, where to find them, and what you need to know to secure your own parcel of land with minimal upfront cost.

Is It Really Possible to Buy Land with No Money Down?

Yes, it is. While the housing market often has rigid financing rules, the market for raw, vacant land is far more flexible. This creates opportunities for buyers who have a steady income but haven't saved the significant down payment that traditional lenders require. The key is to understand the difference between conventional bank financing and more creative, direct-from-seller options.

The Problem with Traditional Bank Loans

Banks and traditional lenders often view raw land as a speculative or risky investment. Unlike a house, vacant land doesn't generate immediate rental income and can take longer to sell. To protect themselves from this perceived risk, banks create significant barriers for land buyers.

Most conventional lenders will demand a down payment of 20% to 50% for a raw land loan, and many won't lend on rural or undeveloped parcels at all. You can learn more about the challenges of conventional land loans to see why so many buyers seek alternative paths to ownership. This high barrier to entry is precisely why seller financing has become such a popular and practical solution.

How No-Money-Down Deals Work

The secret to buying land with little or no money down is finding a seller willing to act as the bank. This arrangement is known as seller financing or owner financing. Instead of you securing a loan from a bank to pay the seller in a single lump sum, the seller allows you to make affordable monthly payments directly to them over an agreed-upon term.

This creates a win-win scenario. The seller receives a reliable stream of income from a property that might otherwise be sitting idle, and you become a landowner without navigating the strict requirements of a traditional mortgage.

In many of these arrangements, the "down payment" is replaced by a small, one-time document fee to cover the cost of preparing the legal paperwork. For example, a land seller like Dollar Land Store might offer a five-acre parcel where the only upfront cost is a small document fee. This model opens the door to land ownership for a wide range of people, including:

- First-time buyers looking for a tangible, affordable asset.

- Outdoor enthusiasts wanting their own private recreational land.

- Families planning for a future homestead.

- Investors seeking to diversify their portfolio with a low-cost property.

Traditional Bank Loans vs. No-Money-Down Options

This table breaks down the main differences between going through a bank and using an alternative like seller financing. It clearly shows why so many people prefer to skip the bank altogether.

| Feature | Traditional Bank Loan | No-Money-Down Methods (e.g., Seller Financing) |

|---|---|---|

| Down Payment | Typically 20-50% of the purchase price. | Often just a small, one-time document fee. |

| Credit Check | Required, with strict FICO score minimums. | No credit check is typically required. |

| Approval Process | Slow and bureaucratic; can take weeks or months. | Fast and simple; often approved the same day. |

| Flexibility | Rigid loan terms and underwriting standards. | Highly flexible; terms are set between buyer and seller. |

| Interest Rates | Based on credit score and market rates. | Often 0% interest or a low, fixed rate. |

| Closing Costs | High; includes appraisal, origination, and title fees. | Very low; usually just a small document fee. |

| Property Type | Often restricted to developed or "buildable" lots. | Can be used for any type of land, including rural and recreational. |

As you can see, no-money-down methods remove nearly all the barriers that stop people from owning land. It’s a simpler, more direct path to making your dream a reality.

Creative Ways to Finance Your Land Purchase

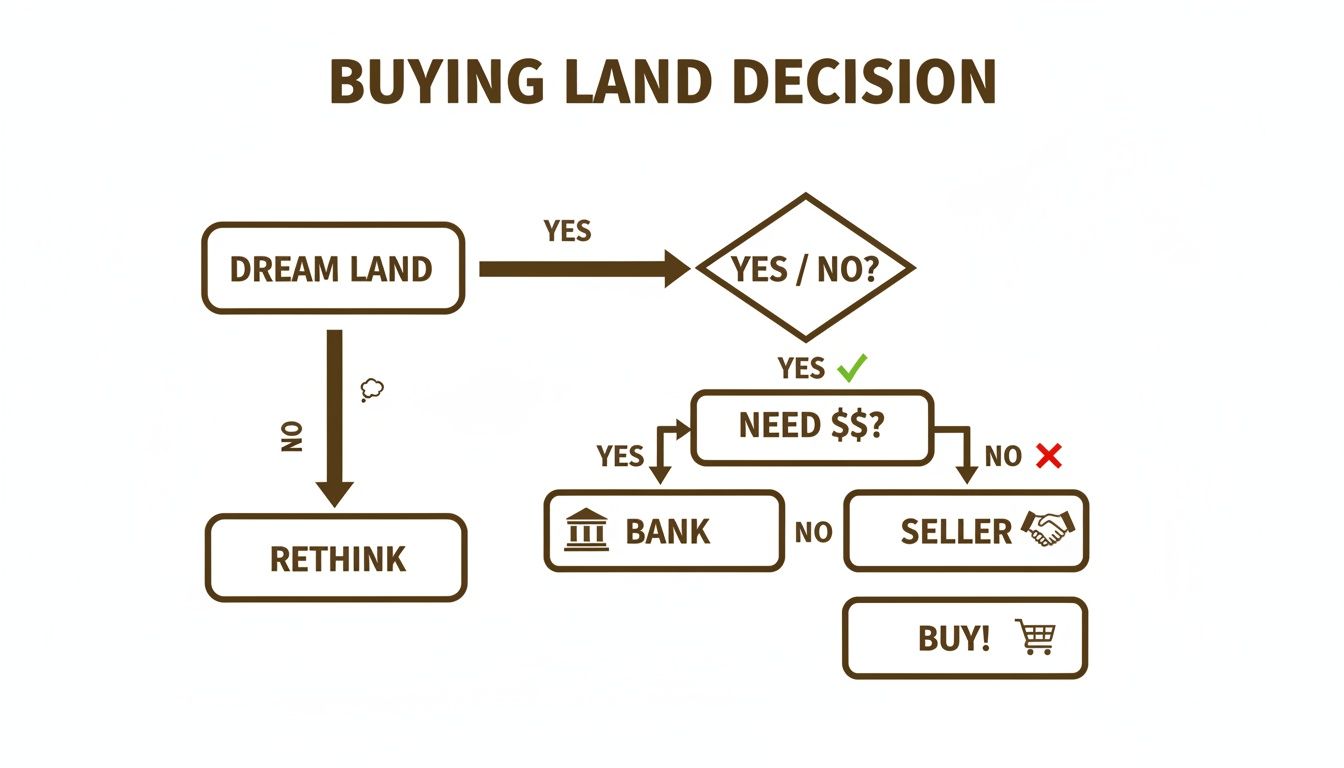

Once you realize you don't need a traditional bank to buy land, a new world of possibilities opens up. The key is learning to work directly with sellers or partners who are open to creative financing, allowing you to bypass restrictive banking rules.

This flowchart illustrates the typical decision process. It shows the two main paths: the traditional bank route with its many hurdles, and the more direct, accessible path of working with a seller.

As the chart suggests, seller financing cuts through much of the red tape associated with conventional loans.

Seller Financing: The Go-To for No-Money-Down Deals

Seller financing, also called owner financing, is the most common and effective way to buy land with little to no money down. Instead of getting a loan from a bank, the property owner becomes the lender. You make your monthly payments directly to them until the land is paid off.

This arrangement works because many landowners, especially those with rural or recreational properties, own their land outright. They are not always seeking a large, immediate cash payout. Instead, they often prefer a steady, predictable monthly income.

You're not just a buyer; you're offering the seller a solution. You are helping them turn a non-income-producing asset into a reliable cash flow stream.

This is the business model that allows companies like Dollar Land Store to operate. We eliminate the middlemen—no loan officers, underwriters, or credit committees are involved. The result is a straightforward agreement between the buyer and the seller. For a more detailed explanation, read our guide on what seller financing is in real estate.

Lease-Purchase Agreements: A “Try Before You Buy” Option

Another useful strategy is a lease-purchase agreement, also known as a rent-to-own or lease-option contract. This arrangement allows you to control and use the land immediately while giving you time to prepare for the final purchase.

Here is how it is typically structured:

- Lease Period: You agree to rent the land for a set term, usually 1 to 3 years, for a fixed monthly payment.

- Purchase Option: The contract grants you the exclusive right to buy the land at a predetermined price.

- Rent Credits: A portion of each rental payment is often credited toward your future down payment or the final purchase price.

This is a great option if you've found the perfect property but need time to save money or improve your financial standing. It allows you to "test drive" the land to ensure it's the right fit before you are fully committed to buying.

Partnerships: Pooling Your Resources

If you have a clear vision but lack the necessary capital, a partnership could be your ticket to land ownership. This involves finding someone who has the money but may not have the time or expertise to find and manage a land deal.

There are two common ways to structure a partnership:

- Equity Partnership: A partner provides the cash for the purchase, while you contribute "sweat equity"—finding the property, conducting due diligence, and perhaps making improvements. You both share in the ownership and any future profits.

- Joint Venture: This is typically a short-term arrangement for a specific goal, such as buying a large parcel to subdivide and sell. One partner provides the funding, the other handles the work, and you split the profits according to your agreement.

The key to a successful partnership is a clear, legally reviewed written agreement. It must define everyone’s responsibilities, ownership stakes, and an exit strategy before any money is spent. This protects all parties and ensures the project runs smoothly.

How to Find and Evaluate No-Money-Down Land Deals

Finding the right property isn't about luck; it's about knowing where to look and what to look for. Uncovering land deals where the seller is open to creative financing is a skill anyone can develop with the right approach.

Where to Find No-Money-Down Land

Opportunities to buy land with no money down are often hiding in plain sight if you focus on the right channels. The goal is to find sellers who value consistent monthly payments more than a large, one-time cash payout.

These sellers often fall into a few common categories:

- Individuals who have inherited land they do not want or need.

- Long-term investors who bought land years ago and are ready to sell without the hassle of a traditional real estate transaction.

- Professional land companies, like Dollar Land Store, that specialize in buying and reselling land with built-in owner financing.

You can find these deals through specialized websites and direct outreach. For more tips, check out our guide on finding cheap rural land for sale. A critical part of the process is learning how to identify finding motivated sellers, as they are far more likely to offer flexible terms.

The current market has also created more opportunities. As rising interest rates have pushed traditional buyers to the sidelines, sellers are more willing to offer financing to attract buyers who can no longer qualify for conventional loans.

The Essential Due Diligence Checklist

Finding a potential no-money-down deal is just the beginning. The next step—due diligence—is what separates a smart investment from a future headache. It is your responsibility to verify every detail about the property before you sign any agreements.

A low price means nothing if the land is unusable. Always verify everything from legal access to zoning regulations. Never take a listing's description at face value without doing your own research.

Your checklist must be thorough. Here are the absolute non-negotiables to investigate for any raw land you are considering.

Confirm Legal and Physical Access

Access is critical. If you cannot legally get to your property, its value is significantly diminished.

- Legal Access: Does the property border a public road? If not, there must be a legally recorded easement granting you the right to cross a neighbor's land to reach yours. A "landlocked" property without a deeded easement is a major red flag.

- Physical Access: Is there a physical road to the property? A legal easement is useless if it crosses a swamp or a steep cliff. Check the road quality and find out if it is maintained year-round, especially in areas with snow.

Investigate Zoning and Land Use Restrictions

You need to know exactly what you are legally allowed to do with the land. Zoning laws are determined at the county level, so you must contact the local Planning and Zoning department for official information.

Ask specific questions based on your intended use:

- Can I build a single-family home?

- Are tiny homes, mobile homes, or manufactured homes permitted?

- What are the rules for camping or parking an RV, and for how long?

- Are there restrictions on off-grid living, such as rainwater collection or solar power systems?

- Is the property part of a Property Owners Association (POA) with its own rules, fees, and restrictions?

Verify Utility Availability

Never assume utilities are available. For rural land, the cost of bringing in power, water, and a septic system can be extremely expensive—sometimes more than the cost of the land itself.

- Water: Is city water available? If not, you will need to drill a well. Contact local well drillers to get an estimate of the average depth and cost in the area.

- Sewer: Can you connect to a city sewer system? If not, you will need a septic system. The county health department can tell you if the soil is suitable for a septic system (this is determined by a "percolation test").

- Power: How far away is the nearest power pole? Extending utility lines can cost thousands of dollars.

- Internet/Cell Service: If you need to stay connected, check the coverage maps for major providers. Verify service yourself when you visit the property.

This research process ensures that the deal you found isn't just affordable upfront—it's a sound, usable investment for your future.

Navigating the Paperwork and Closing Process

Once your due diligence is complete and you've agreed on terms with the seller, it's time to make the deal official. The good news is that the paperwork for a seller-financed land deal is typically much simpler and more straightforward than a traditional closing, which is a significant relief for first-time buyers. Instead of a mountain of bank documents, the process usually involves just a few key agreements that create a clear, legally sound record of the transaction.

Key Documents You Will Encounter

In a seller-financed purchase, the entire agreement is laid out in a few core documents. While the names may vary slightly, these are the essential agreements you should expect to see.

- Purchase Agreement: This is the initial document that formalizes the deal. It includes the property's legal description, the agreed-upon purchase price, the payment schedule, the interest rate (if any), and the responsibilities of both the buyer and seller.

- Promissory Note: This is your written promise to repay the loan according to the agreed-upon schedule. It specifies the total amount owed, the monthly payment amount, and the loan term.

- Land Contract (or Contract for Deed): This is the central document in most seller-financed deals. It states that the seller retains legal title to the property while you, the buyer, receive equitable title. This gives you the right to use and enjoy the land. Once the final payment is made, the seller transfers the legal title to you via a deed.

The Land Contract is designed to protect both parties. It gives you the security of knowing you have a legal right to the land as long as you make your payments, and it protects the seller by allowing them to reclaim the property if you default.

Reputable sellers like Dollar Land Store use standardized, easy-to-understand contracts to ensure transparency. This clarity eliminates guesswork and ensures you know exactly what you are agreeing to, with no hidden clauses or confusing jargon. While it's possible to learn how to buy land without a realtor, a well-written contract is your most important tool in any transaction.

Understanding The Closing Process

Forget the complex closings associated with banks, which often involve expensive title companies and attorneys. A direct sale from a seller is much simpler. Often, the "closing" is just the act of signing the purchase documents and making your initial payment, which may only be a small document fee. A basic understanding banking processes can be helpful for setting up automatic payments.

After signing, the most important step is recording the sale with the county. Some sellers handle this for you, but it may be your responsibility. Recording the Land Contract (or a summary of it) at the county recorder’s office creates a public record of your interest in the property, which is crucial for protecting your ownership rights against future claims.

This simplified process is a major advantage of buying directly from a company specializing in owner financing. It eliminates many of the fees and delays associated with bank loans, getting you closer to owning your own land, faster.

What This Means for Buyers

For anyone who thought land ownership was out of reach, understanding these no-money-down strategies changes everything. It means that with a steady income and a clear plan, you can become a landowner without needing tens of thousands of dollars in savings.

The key takeaway is that the raw land market operates differently than the residential housing market. Motivated sellers and specialized land companies have created a more accessible path to ownership. By using seller financing, you can bypass the biggest hurdles—credit checks and large down payments—and secure a tangible asset that you can use and enjoy for years to come.

This approach puts you in control. Instead of trying to fit the rigid criteria of a bank, you can find a seller whose terms work for you. It democratizes land ownership, making it a realistic goal for first-time buyers, families, and anyone looking for a piece of the American dream.

Why Consider Dollar Land Store?

When you’re looking to buy land with little to no money down, the seller you choose is just as important as the financing strategy. At Dollar Land Store, our entire business was built to solve the biggest problems aspiring landowners face: high upfront costs and complicated, intimidating purchase processes. We are not a traditional real estate agency; we are a direct seller of affordable, undeveloped land, and we specialize in making ownership straightforward and accessible.

Our model is centered on providing high-quality raw land with simple owner financing. This means you get to skip the banks, credit checks, and rigid requirements. We believe your credit history shouldn't prevent you from owning property, which is why we offer financing to everyone.

Here’s what makes the Dollar Land Store experience different:

- Affordable Land with Low Payments: We've removed the biggest barrier to entry. Instead of a 20-50% down payment, most of our properties only require a small, one-time document fee to get started.

- Simple Owner Financing with No Credit Checks: Our financing is straightforward. We don't run credit checks, and our approval process is fast and simple.

- Transparent Terms: Every property listing clearly shows the purchase price, document fee, and estimated monthly payment. There are no hidden fees or last-minute surprises.

- No Middlemen or Real Estate Agents: You work directly with us, the owner. This eliminates realtor commissions and streamlines the entire transaction.

- Broad Inventory Across Several States: We offer a wide selection of parcels in multiple states, giving you real choices for a weekend getaway, a future homestead, or a long-term investment.

- Fast Contract Setup: Our process is so efficient that you can often review and sign all necessary paperwork online in a single day, securing your land quickly.

At Dollar Land Store, our mission is to transform the complicated goal of buying land into a simple, achievable reality. We provide the properties and the financing so you can focus on bringing your dream to life.

Next Steps: Your Path to Land Ownership

You now understand the strategies for buying land with little or no money down. It's time to move from planning to action. The journey to land ownership begins with a few clear, deliberate steps.

1. Define Your Goals

Before you look at a single listing, clarify what you are really looking for. This will save you countless hours of searching.

- What Is Your "Why"? Are you looking for a weekend camping spot, a long-term investment, or a future off-grid homestead? Your primary goal will shape every decision.

- What Is Your Monthly Budget? Focus on a monthly payment you can comfortably afford without financial strain. This should be an exciting investment, not a burden.

- What Are Your Non-Negotiables? Make a short list of 3-5 absolute must-haves. Do you need year-round road access? Specific zoning for a tiny home? Proximity to a certain town?

2. Start Your Search

With a simple plan, you're ready to see what opportunities are available. The most direct way to start is by browsing owner-financed properties where the terms are simple and transparent.

- Browse available land at DollarLandStore.com. Explore our listings in the states that interest you and see how the prices and monthly payments align with your budget.

- Ask questions. If you have questions about a specific property or want to understand our financing process better, contact us. Our team is here to provide clear, straightforward answers to help you move forward with confidence.

Your piece of land is out there. Taking the first step is all that's required to begin your journey.

Conclusion

Buying land with no money down isn't just a fantasy—it's a practical and achievable goal for anyone with a clear plan and the right strategy. By leveraging seller financing, you can bypass the restrictive and expensive requirements of traditional banks and secure your own piece of property with minimal upfront cost. The key is to conduct thorough due diligence, understand the terms of your agreement, and partner with a trustworthy seller who makes the process transparent and simple.

With these tools and insights, you are now equipped to turn your dream of land ownership into a reality.

Ready to find a property with clear, upfront terms? Browse available land at DollarLandStore.com.