Your Guide to No Credit Check Land Loans and Seller Financing

Ross AmatoBuying your own piece of land without needing approval from a traditional bank is possible through a no-credit-check land loan, an approach more commonly known as seller financing or owner financing. This is a direct agreement between you, the buyer, and the seller of the property, making the process of becoming a landowner much more accessible.

This guide explains how these loans work, what the process looks like, and why they are a practical option for first-time land buyers.

What Are No-Credit-Check Land Loans?

A no-credit-check land loan removes the traditional lender—like a bank or credit union—from the land buying process. Instead of submitting extensive applications, income verification, and having your credit score analyzed, you work directly with the property owner.

In this arrangement, the seller acts as the lender. You and the seller agree on a purchase price, a down payment, and a monthly payment schedule. You then make these payments directly to the seller over an agreed-upon term. The land itself serves as collateral for the loan, which means if a buyer defaults on payments, the seller can reclaim the property. For a beginner, this straightforward method can make buying land far less intimidating.

How Is This Different from a Bank Loan?

The primary difference lies in the approval criteria. Banks and traditional lenders focus heavily on your credit history to assess risk. A low credit score, limited credit history, or non-traditional income can often lead to a denial.

Sellers offering financing are typically concerned with two simpler factors:

- A reasonable down payment: This shows you are a serious buyer and have a vested interest in the property.

- Your ability to make the monthly payments: Payments are usually fixed, predictable amounts that are easy to budget for.

Because the seller owns the land outright, they have the flexibility to set their own financing terms. This creates a path to land ownership for individuals who may not meet the strict requirements of conventional lenders. Our guide on how to finance a land purchase explores these different options in greater detail.

Why This Is a Practical Option for First-Time Land Buyers

Seller financing provides a viable opportunity for many aspiring landowners. Traditional lenders often require credit scores of 700 or higher for land loans. With seller financing, buyers with lower scores can often still purchase property. This is a significant advantage, as many people have credit profiles that would automatically disqualify them from a conventional bank loan.

For many people dreaming of owning property, seller financing isn’t just another option—it can be the most practical path forward. It replaces the complexities of credit checks with a simple, direct agreement.

This approach helps create opportunities for individuals with non-traditional income, those who have faced past financial challenges, or those who simply haven't had the chance to build an extensive credit history. It is a functional and accessible way to acquire property, based on a clear understanding between buyer and seller.

How The Seller Financing Process Works

The process for a no-credit-check land loan is typically much simpler and faster than a conventional bank loan. By creating a direct agreement between you and the seller, it eliminates much of the administrative overhead.

It begins when you find a property that offers seller financing. The listing should clearly state the key terms: the total purchase price, the required down payment, the interest rate (if any), and the monthly payment amount. This transparency helps ensure there are no surprises later.

Once you find a parcel that fits your budget and goals, the next step is to formalize the agreement.

Key Documents in Seller Financing

Unlike a bank loan that involves extensive paperwork, seller financing usually relies on a few core documents. These are legally binding contracts designed to protect both the buyer and the seller.

You will typically encounter three main documents:

- Purchase Agreement: This is the initial contract outlining the fundamental terms of the sale, including the price, financing details, and closing date.

- Promissory Note: This document is your formal "IOU." It specifies the total loan amount, interest rate, payment schedule, and the consequences of missed payments.

- Land Contract or Deed of Trust: This is a critical agreement stating that the seller retains the legal title to the property while you make payments. It also affirms your right to use and enjoy the land according to the terms of the agreement.

This streamlined process involves fewer parties, which means less waiting and potentially lower closing costs. To learn more about how these elements work together, read our detailed guide on what seller financing is in real estate.

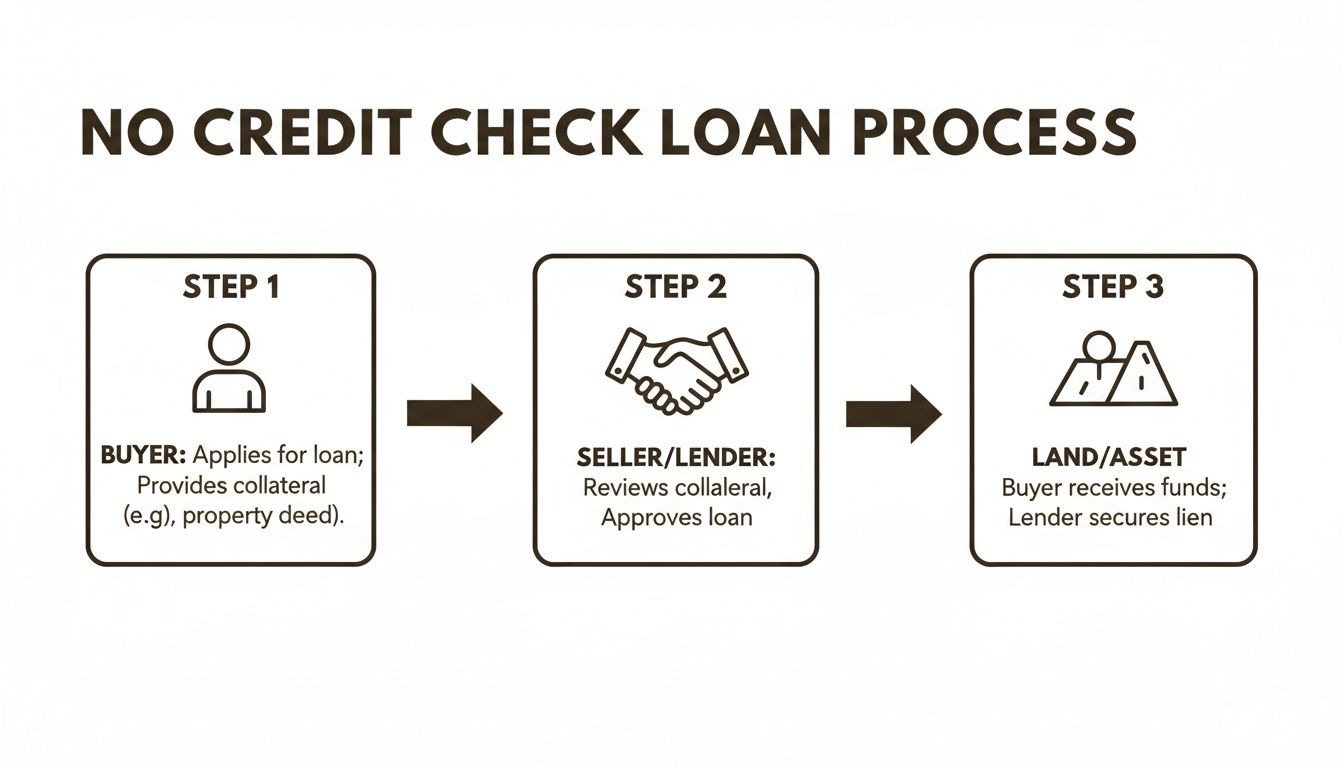

This simple graphic shows the direct flow of the process.

As shown, it's a direct, three-step relationship: you find the land, agree on terms with the seller, and begin your journey toward ownership.

Securing The Property and Receiving The Deed

Once the documents are signed and the down payment is made, the property is secured in your name. You can typically begin using the land immediately, according to the agreed-upon terms. From that point on, you continue making monthly payments directly to the seller for the duration of the loan.

The most significant moment in this process is making the final payment. Once the loan is paid in full, the seller is legally obligated to transfer the property’s deed to you.

Receiving the deed is a major milestone—it signifies that you officially own the land free and clear. The seller signs it over, and you file it with the appropriate county office. This action makes your ownership a matter of public record, officially completing the purchase.

Seller Financing Versus Traditional Bank Loans

Understanding your financing options is crucial when buying land. To help clarify the best path for your situation, let’s compare seller financing with a conventional bank loan. We will examine the practical differences in credit requirements, down payments, approval times, and overall complexity.

Seller financing removes much of the administrative delay. Transactions can often be completed in days, not the months it can take with a bank. Banks operate under a different set of regulations, requiring high credit scores, substantial paperwork, and additional costs like appraisal and origination fees.

This comparison is intended to provide a clear picture, weighing the efficient route of seller financing against the more rigid process of a traditional bank loan.

Comparing Key Differences

To fully understand what separates these two financing methods, let's break down the factors that matter most to buyers. The table below illustrates what you can generally expect from each approach.

Seller Financing vs. Traditional Bank Land Loans

Here is a straightforward comparison of the core differences between financing directly from a seller versus a bank.

| Factor | Seller Financing (No Credit Check) | Traditional Bank Loan |

|---|---|---|

| Credit Requirement | None. Credit history is not typically a factor in approval. | A high score is often required, usually 680-700+. |

| Approval Speed | Fast. Approval can happen in hours, with closing in days. | Slow. Expect a 30-45 day underwriting process or longer. |

| Down Payment | Often low. It may be a small fixed amount or a low percentage. | High. Banks commonly require 25% to 50% of the purchase price. |

| Paperwork | Minimal. Typically a purchase agreement and promissory note. | Extensive. Requires tax returns, pay stubs, bank statements, and more. |

| Additional Costs | Few. A small document fee may apply. | Many. Includes appraisal fees, origination fees, and other closing costs. |

| Flexibility | High. Terms can often be discussed directly with the seller. | Low. Bank terms are typically rigid and non-negotiable. |

This table highlights a fundamental difference in approach. Seller financing is structured to make land ownership more accessible, whereas banks are focused on minimizing risk through strict, standardized requirements.

The Impact on Accessibility and Cost

The stringent requirements of banks can exclude many potential buyers from the market. For instance, a significant portion of the population has credit scores below the typical minimum required for a conventional loan. These individuals are likely to be denied or offered very high interest rates, sometimes 12% to 15% or more.

No-credit-check land financing provides an alternative for these same individuals, often with more reasonable interest rates, typically between 6% and 12%. Furthermore, many sellers are willing to work with buyers to establish a monthly payment that fits their budget—a level of flexibility not usually found with large financial institutions.

The core advantage of seller financing is its simplicity. It removes the institutional barriers that can prevent aspiring buyers from owning land, focusing instead on a direct agreement between two parties.

The down payment is another significant hurdle with banks. As you evaluate your options, it's important to know what you will be expected to pay upfront. You can learn more by reading our guide on how much of a down payment for land is typically required. It illustrates how seller financing can significantly lower this initial barrier, allowing you to secure land with less cash. This approach not only saves time but also reduces the stress and uncertainty often associated with obtaining a bank loan.

Weighing the Pros and Cons of Seller Financing

Like any financial decision, no credit check land loans come with their own set of advantages and potential drawbacks. While seller financing offers a direct and accessible path to land ownership, it is important to consider both sides to determine if it aligns with your financial goals and comfort level.

For many buyers, the benefits directly address the most common obstacles in the land market.

Advantages of Seller Financing

The primary advantage is accessibility. Seller financing makes land ownership possible by removing the traditional gatekeepers—the banks.

- No Credit History Required: Your credit score or past financial challenges do not prevent you from buying land.

- Faster Closing Process: Without underwriters, appraisers, and loan committees, the timeline is significantly shorter. You can often complete a purchase in days instead of months.

- Lower Upfront Costs: Banks often require a down payment of 25% to 50% for raw land. With seller financing, the down payment is typically much smaller and more manageable.

- Simplified Paperwork: The process is built on a few straightforward agreements, such as a purchase contract and a promissory note, rather than the extensive documentation required by banks.

These factors make owning land a realistic goal for people who might otherwise be excluded. Conventional land loans often require credit scores in the high 600s or 700s and have strict debt-to-income ratios that can be challenging for self-employed buyers or those with variable incomes. Seller financing bypasses these hurdles. You can learn more about conventional land loan requirements on LendingTree.com.

Potential Drawbacks to Consider

While the advantages are significant, it is equally important to be aware of the potential drawbacks. Understanding these helps ensure you make an informed decision.

- Potentially Higher Interest Rates: Because the seller is taking on the risk that a bank would not, the interest rate may be slightly higher than what someone with excellent credit could obtain through a traditional loan. This is often the trade-off for the convenience and accessibility offered.

- The Seller Retains the Title: In most seller financing arrangements, the seller holds the legal title to the property until the final payment is made. This is a standard practice to protect the seller's investment. As the buyer, you hold "equitable title," which grants you the right to use and enjoy the land as specified in your contract. Upon full payment, the legal title is transferred to you.

- Risk of Unfavorable Terms: Due diligence is critical. It is essential to carefully read your contract and watch for clauses like balloon payments—a large, lump-sum payment due at the end of the loan term. Reputable sellers, like Dollar Land Store, offer clear, fully amortized loans without such terms, but it is a factor to be aware of when evaluating any seller-financed offer.

When you weigh these pros and cons, a clear picture emerges. Seller financing prioritizes speed and accessibility, which may come at the cost of a slightly higher interest rate. For many, this is a reasonable trade-off to begin building equity in a tangible asset today.

What This Means for Buyers

Understanding the mechanics of no-credit-check loans is one thing, but what does it mean for you in practice? If you are a first-time land buyer, this financing method offers a direct path to owning a tangible asset without navigating the traditional financial system.

It allows you to invest in land for recreation, a future home, or as a long-term asset without needing a perfect credit score. The focus shifts from your financial past to what you can comfortably afford in the present.

You Are in Control of the Timeline

One of the most significant differences you will experience is the speed and control you have over the process. Instead of waiting weeks or months for a bank's decision, seller financing puts you in the driver's seat. You can find a property you like and secure it quickly, allowing you to start building equity immediately.

This means you are less likely to miss out on a desirable property while waiting for a lengthy loan approval process. The main consideration becomes finding a monthly payment that fits your budget.

The Importance of Buyer Due Diligence

While seller financing simplifies the purchasing process, it places more responsibility on you, the buyer. Since there is no bank requiring appraisals or detailed property reports, it is up to you to conduct this essential research. This process is often called "due diligence."

Before purchasing, be sure to verify key details with local county authorities:

- Access: Confirm that there is legal and physical access to the property.

- Zoning: Contact the county to ensure the land can be used for your intended purpose (e.g., residential, recreational).

- Property Taxes: Inquire about the annual property tax amount to avoid future surprises.

This responsibility is empowering. It encourages you to become a more informed and engaged buyer, leading to a deeper understanding of your property and greater confidence in your purchase.

Ultimately, a no-credit-check land loan is about taking control of your financial future on your own terms. To better understand the value of your purchase, it can be helpful to learn how to calculate your return on investment. This can help you view your land not just as a piece of property, but as a strategic investment in building long-term wealth.

Why Consider Dollar Land Store?

Understanding the concept of seller financing is helpful, but seeing it in practice provides real clarity. At Dollar Land Store, the no credit check land loan model is not just a theoretical concept—it is the foundation of our business. We are not brokers or agents; we own every parcel of land we sell.

This direct ownership allows us to offer our own in-house financing, which removes middlemen and simplifies the entire process, particularly for first-time buyers.

A Process Designed for Simplicity

Our primary goal is to remove the common barriers that prevent people from owning land. Because we manage the entire process, there is no need to involve banks, undergo lengthy credit approvals, or submit to invasive background checks. This significantly accelerates the purchase timeline.

Here is what makes our approach different:

- Direct In-House Financing: We provide the financing directly, creating a simple and clear agreement between us and you.

- No Credit or Background Checks: Your financial history does not determine your ability to purchase land from us. We believe everyone deserves the opportunity to become a landowner.

- Transparent and Clear Terms: Each property listing clearly details the total price, down payment, and fixed monthly payment. You will never encounter hidden fees or balloon payments.

Making Land Ownership More Accessible

By removing middlemen, we also eliminate unnecessary complexity and costs. Our streamlined system makes it easier for people to buy land for recreation, investment, or a future homesite without the hurdles of traditional lending.

The entire Dollar Land Store model is built to be a straightforward and trustworthy option for anyone who decides that seller financing is the right path for them.

We focus on making your land purchase as transparent and efficient as possible. All important information is provided upfront, so you can make a decision with confidence. It's a practical, no-nonsense path to owning your own piece of land, built on a foundation of honesty and direct communication.

Buyer Guidance and Next Steps

You now have a foundational understanding of how no credit check land loans work and can make an informed decision for your future. The next step is to turn this knowledge into action.

A good starting point is to simply browse available properties. This is a low-pressure way to see what is available in the market, what fits within your budget, and how a transparent seller presents pricing and financing terms.

Turning Knowledge into Action

Your journey to land ownership can begin today. Here are a few practical steps you can take to move forward:

- Conduct Your Due Diligence: Before committing to a purchase, it is vital to research the property thoroughly. Our guide on what to look for when buying land provides a helpful checklist to get you started.

- Plan Ahead: Owning land is the first step. Consider what it will take to prepare the property for your plans. Resources like excavation and land clearing guides can provide insight into what that process might involve.

- Ask Questions: If you have questions about a property, do not hesitate to ask. A reputable seller will provide straightforward answers without high-pressure sales tactics.

This is where your research comes together. By taking these practical steps, you can feel confident and secure in your decision to become a landowner.

Conclusion

No-credit-check land loans, or seller financing, offer a direct and accessible path to property ownership. By removing traditional lenders from the process, this approach eliminates the need for credit checks, reduces paperwork, and allows for faster closings. While it's important to conduct thorough due diligence and understand the terms of your agreement, seller financing provides a practical solution for many aspiring landowners.

This model empowers you to invest in a tangible asset and take control of your financial future, regardless of your credit history. With a clear understanding of the process, you can confidently take the next steps toward owning your own piece of land.

Ready to take the next step?