No Credit Check Land Financing: The Ultimate Buyer's Guide

Ross AmatoImagine buying a piece of land without ever stepping into a bank or worrying about your credit score. That’s exactly what no credit check land financing offers—a direct, practical path to owning property where the seller provides the loan. The focus isn't on your credit history, but on your ability to make the payments.

This guide explains how this financing model works, what its pros and cons are, and how first-time buyers can use it to secure their own piece of land.

What No Credit Check Land Financing Really Means

At its core, no credit check land financing is a type of seller financing. It is a straightforward agreement between you and the property seller. The seller acts as the lender, allowing you to pay for the property in affordable installments over time. This approach is also commonly known as owner financing.

This method sidesteps the common roadblocks of conventional lending. Banks and credit unions are often cautious when it comes to financing raw land, typically requiring extensive paperwork, high credit scores, and long approval processes. For many people, especially first-time buyers or those with imperfect credit, these hurdles can make owning land seem out of reach.

Bank Loans vs. Seller Financing at a Glance

It is helpful to see the two approaches side-by-side to understand the key differences.

| Factor | Traditional Bank Loan | No Credit Check Seller Financing |

|---|---|---|

| Credit Check | Required, often with a high score (670+) | Not required |

| Approval Process | Slow, complex, and bureaucratic | Fast and simple, often same-day |

| Down Payment | Typically high, often 15% to 25% or more | Low, sometimes just a few hundred dollars |

| Documentation | Extensive (tax returns, pay stubs, bank statements) | Minimal (basic ID and income verification) |

| Flexibility | Rigid terms set by the institution | Flexible terms negotiated with the seller |

| Accessibility | Limited to those with excellent credit and finances | Open to almost everyone, regardless of credit history |

As you can see, seller financing is designed for accessibility and speed, making land ownership a real possibility for a wider range of people.

What Sellers Look For Instead of a Credit Score

Instead of pulling a detailed credit report, sellers using this model focus on practical factors. They want to ensure you are a reliable buyer and typically confirm this by looking at:

- A stable source of income: This shows you can comfortably afford the monthly payment.

- A reasonable down payment: This demonstrates your commitment to the purchase.

- A simple purchase agreement: The terms, interest rate, and payment schedule are all laid out clearly in a contract between you and the seller.

This model opens the door to land ownership for more people. Traditional lenders often look for high credit scores and their down payment requirements can be a significant barrier.

By focusing on your ability to pay today—not your financial past—this financing method creates a legitimate and accessible path to owning your own piece of land.

To learn more about this process, our guide on what is seller financing in real estate offers a deeper look. The goal is to create a direct, transparent, and more attainable route to buying land.

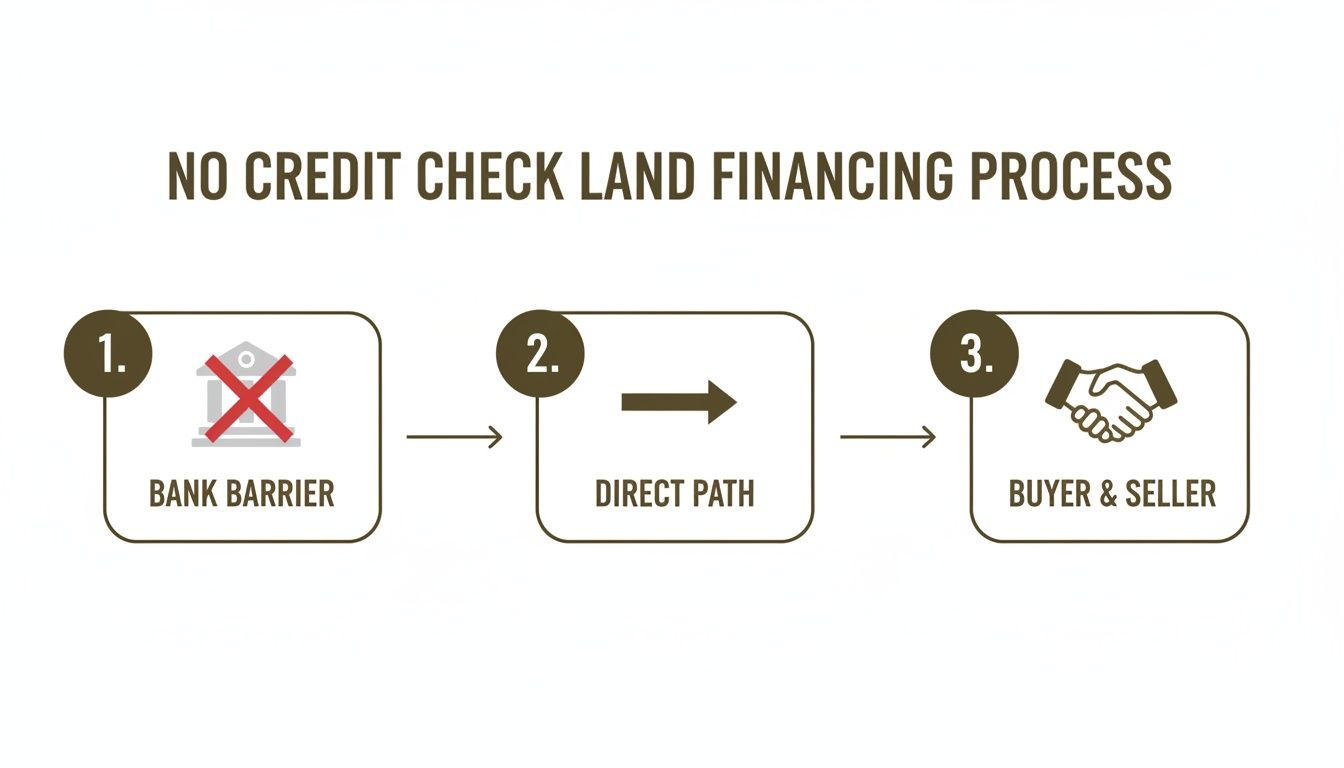

How The Seller Financing Process Works

The process of securing a traditional bank loan involves extensive paperwork, long waiting periods, and strict credit approvals. Buying land with seller financing is different. It’s far more direct because you work one-on-one with the seller, eliminating the middleman and typical banking bureaucracy.

This simplified path gets you from finding a property to calling it your own much faster.

This visual shows just how straightforward it is. You're creating a direct line to the seller, completely bypassing the barriers and red tape that banks put up.

As you can see, the journey is just between you and the seller. No loan committees, no underwriters—just a simple, direct agreement. Let’s walk through what that looks like, step-by-step.

Step 1: Find a Property

Your first move is to find a piece of land where the seller offers financing. On our listings at Dollar Land Store, for example, you’ll see everything laid out clearly—the total price, the down payment needed, and what your monthly payments will look like.

Step 2: Review the Terms

Once you've selected a property, it's time to review the terms of the agreement. This is usually simple and includes a few key details:

- Purchase Price: The total cost for the land.

- Down Payment: The initial amount you’ll pay to secure the property.

- Interest Rate: The percentage charged on the remaining balance.

- Loan Term: How long you have to pay off the loan (e.g., 5, 10, or 15 years).

- Monthly Payment: The fixed amount you'll pay every month.

All these details are spelled out in a Purchase Agreement. This is typically a concise document written in plain language that is easy to understand.

Step 3: Make It Official

If you are satisfied with the terms, the next step is to sign the purchase agreement and make your down payment. A credit check is not part of this process. The main focus is ensuring you have a reliable way to handle the monthly payments. The entire process often happens online and can be completed in just a few hours or days.

Step 4: Sign the Closing Documents

The final step is signing the legal documents. In seller financing, this is often a Land Contract, also known as a Contract for Deed.

A Land Contract is a straightforward legal agreement. The seller holds the official property title while you make payments. In return, you get "equitable title," which gives you the right to use, enjoy, and improve the land as if you own it, as long as you keep up with your payments.

Once you make the final payment, the legal title is officially transferred to your name. The entire process is designed for speed and clarity.

To dig a little deeper into how this works, check out our complete guide to owner-financed land for sale.

Weighing the Pros and Cons of This Approach

To decide if no credit check land financing is right for you, it is important to look at it from all sides. This path to owning land has significant advantages, especially for first-time buyers, but it also comes with specific responsibilities. Understanding both will help you determine if this method aligns with your goals.

The biggest benefit is accessibility. It opens the door for people who might be turned away by a traditional bank—individuals with less-than-perfect credit, the self-employed, or anyone who prefers to avoid the extensive paperwork of a typical loan.

The Clear Advantages for Buyers

For many aspiring landowners, the benefits are what make land ownership possible. They remove the common hurdles that can make buying land seem difficult.

Here’s what stands out:

- No Credit History Barrier: Your credit score is not a factor in the approval process. The seller focuses on your ability to make the monthly payments.

- Faster and Simpler Closings: The deal can often be completed in a matter of days, not the weeks or months a bank loan typically takes.

- Lower Upfront Costs: Down payments are often much smaller than the 15-25% that banks usually demand for a raw land loan.

- More Flexible Terms: Some sellers are willing to work with you on payment schedules or terms in a way a large institution would not.

Potential Risks and Considerations

While the upsides are clear, this approach places more responsibility on the buyer. Since there’s no bank conducting its own checks, the task of performing thorough research—known as due diligence—falls entirely on you.

Keep these points in mind:

- Higher Interest Rates: To balance the risk of not performing a credit check, sellers often charge a higher interest rate than a bank would. This is a common trade-off for the convenience and accessibility offered.

- Buyer Assumes All Due Diligence: You are responsible for verifying all details, including legal access, zoning regulations, and ensuring the property title is clear.

- The Seller Holds the Title: With a Land Contract, the seller retains legal title to the property until the loan is fully paid. You receive equitable title, which grants you the right to use and enjoy the land, but the deed is not transferred to your name until the final payment is made.

This table provides a simple comparison to help you weigh your options.

Advantages vs. Potential Risks for Buyers

| Pros (Advantages for the Buyer) | Cons (Potential Risks to Consider) |

|---|---|

| Simple Approval: No credit check means past financial issues won't prevent you from buying. | Higher Interest Rates: You will likely pay a higher rate to offset the seller's risk. |

| Fast Process: Close on your land in days, not the typical weeks or months. | Full Due Diligence Burden: All research (access, zoning, title) is your responsibility. |

| Low Down Payments: Get started with much less cash upfront than a bank requires. | Seller Retains the Deed: The seller holds the legal title until the loan is fully paid. |

| Flexible Terms: Sellers can often offer more personalized payment arrangements. | Fewer Legal Protections: Owner financing is governed by different rules than standard mortgages. |

Ultimately, it’s about balancing the immediate opportunity against the long-term responsibilities. For many, it's a perfect fit.

Owner financing has become a popular alternative to traditional lending. By eliminating bank fees and complex applications, it has made land ownership a reality for many people. Interest rates for these arrangements typically range between 6% to 12%. You can learn more by reading these insights on owner financing options on scprgv.com.

No credit check land financing is a powerful tool that creates a straightforward path to property ownership by prioritizing accessibility over credit scores.

Your Essential Due Diligence Checklist

When you choose no credit check land financing, you skip the bank’s lengthy approval process. This also means you are responsible for all the research. There is no loan officer requiring appraisals, surveys, or title searches. It's all up to you.

This freedom is empowering, but it requires you to be thorough.

Running through a simple checklist helps ensure the land you are considering can meet your needs and expectations.

Property Verification and Access

First, confirm the basics. Getting these fundamentals right from the start can prevent significant issues later.

- Confirm Ownership and Title: Your first call should be to the county recorder or clerk’s office. You need to verify that the person selling the land is the legal owner on record.

- Check for a Clear Title: Ask the seller if the title is free of any liens or claims. A "clear title" means no one else can claim a right to your property.

- Verify Legal Access: Do not assume a visible road provides legal access to your land. Contact the county’s planning or road department and confirm the property has deeded, legal access. This is critical.

- Review Property Taxes: A quick call to the county tax assessor can tell you if the property taxes are current. You do not want to inherit someone else's tax bill.

Understanding Land Use and Restrictions

Next, determine what you can legally do with the land. Every county has its own set of rules, so never make assumptions.

A common mistake for first-time buyers is assuming a rural parcel has no restrictions. Zoning laws, deed restrictions, and local ordinances exist everywhere and dictate everything from building sizes to whether you can park an RV.

The best way to get accurate answers is to call the county’s Planning and Zoning Department. Have the parcel number (APN) ready and ask direct questions about your plans:

- What is the property’s current zoning classification (e.g., residential, agricultural)?

- Are there any restrictions on building, camping, or mobile homes?

- What are the setback requirements (how far from property lines structures must be)?

- Are there any major development projects planned for the surrounding area?

Doing this homework upfront ensures your vision for the land aligns with local regulations. For a deeper dive into this crucial step, read our guide on what to look for when buying land. Performing your due diligence is the most important part of making a land purchase you will feel good about for years to come.

What This Means for First-Time Land Buyers

For those new to buying land, no credit check financing is more than just a payment method—it’s a way to overcome the biggest obstacle that prevents many people from owning property: the high standards set by traditional banks. This approach makes land ownership a realistic goal for a much broader audience.

This model provides a clear path to owning a real, tangible asset for people who are often excluded from conventional loans.

Who Benefits Most From This Approach?

- Self-Employed Individuals: If your income doesn't fit into a conventional W-2 format, you can avoid the extensive paperwork banks require to verify earnings.

- People Rebuilding Credit: A past financial challenge or a low credit score won't automatically disqualify you from buying land.

- First-Time Buyers: It's a simpler and less intimidating way to enter the real estate market without complex forms and processes.

- Anyone Who Values Simplicity: If you prefer to avoid the slow, bureaucratic process of a typical bank loan, this direct approach is significantly faster.

The core idea is simple: your financial past should not stop you from building your future. No credit check financing evaluates your ability to make payments today, not just a historical credit score.

For first-time buyers, this means you can act now. Instead of spending years saving to meet a bank’s steep 20-25% down payment requirement, you can often secure a property with a much smaller upfront amount. You can start building equity and enjoying your land right away, whether for a weekend getaway, a future home site, or a long-term investment. It transforms land ownership from a distant dream into a manageable, step-by-step reality.

To see how straightforward the process can be, explore our guide on buying plots of land.

Why Consider Dollar Land Store?

Understanding how no credit check financing works is one thing; finding a seller who operates on those principles is another. At Dollar Land Store, our entire business is built on making land ownership simple and accessible. We are not brokers or agents listing properties for others—we own every parcel of land we sell.

Being the direct seller simplifies the entire transaction. It means no middlemen, no commissions, and a much cleaner, faster path to owning your property. Our goal is to make land ownership a real possibility for everyone, regardless of their credit score or experience with real estate.

Our business is centered on offering affordable raw land with owner financing that is easy to understand. When you look at one of our listings, you see the total price, the down payment, and the monthly payment clearly stated. There are no hidden fees or surprises.

This commitment to transparency extends to our contracts, which are written in plain language. We have structured our process to address the questions and concerns of first-time buyers, making the entire journey as smooth as possible. With inventory across multiple states, Dollar Land Store provides a straightforward and trustworthy way to find and purchase your own piece of land. To learn more, explore the market trends on YouTube and see how the market for owner-financed land has grown.

Buyer Guidance and Next Steps

To wrap things up, let's go over a few of the questions we hear most often from first-time land buyers. Having clear answers can provide the confidence you need to move forward.

Is Seller Financing For Land a Safe and Legal Option?

Yes, absolutely. Seller financing is a legitimate and widely used method for buying real estate across the country. The key to ensuring a safe transaction is a clear, legally sound written contract. This document outlines all the terms and is signed by both you and the seller, protecting everyone involved.

Can I Pay Off My Land Loan Early Without a Penalty?

With most reputable sellers, including Dollar Land Store, you can pay off your loan early without any prepayment penalties. This flexibility allows you to pay off your property whenever you are ready, which can save you money on interest. Always confirm this detail in your purchase agreement before signing.

What Happens if I Miss a Payment?

Every agreement includes a "default clause" that explains what happens if payments are missed. In a worst-case scenario, you could forfeit the property and any money already paid. Communication is critical. If you anticipate having trouble making a payment, contact the seller. Open and honest dialogue can often resolve issues before they escalate.

A Note on Legal Advice: Although not always required, having a real estate attorney review your contract is a prudent step. They can ensure you fully understand the terms and provide valuable peace of mind.

Conclusion

No credit check land financing removes traditional barriers to property ownership, making it an accessible option for many people. It offers a faster, simpler process with lower upfront costs compared to conventional bank loans. However, it also places the responsibility of thorough due diligence squarely on the buyer. By understanding the process, weighing the pros and cons, and carefully researching a property, you can confidently take the first step toward owning your own piece of land.

Ready to find your own piece of land with a straightforward financing process?